Jump to a Policy Topic

Policy Issues

NBWA educates local and federal officials and regulators on the value of state-based alcohol regulation as well as the economic and regulatory issues that impact America’s beer distributors, who are local family-owned businesses that service every state and congressional district throughout the United States.

-

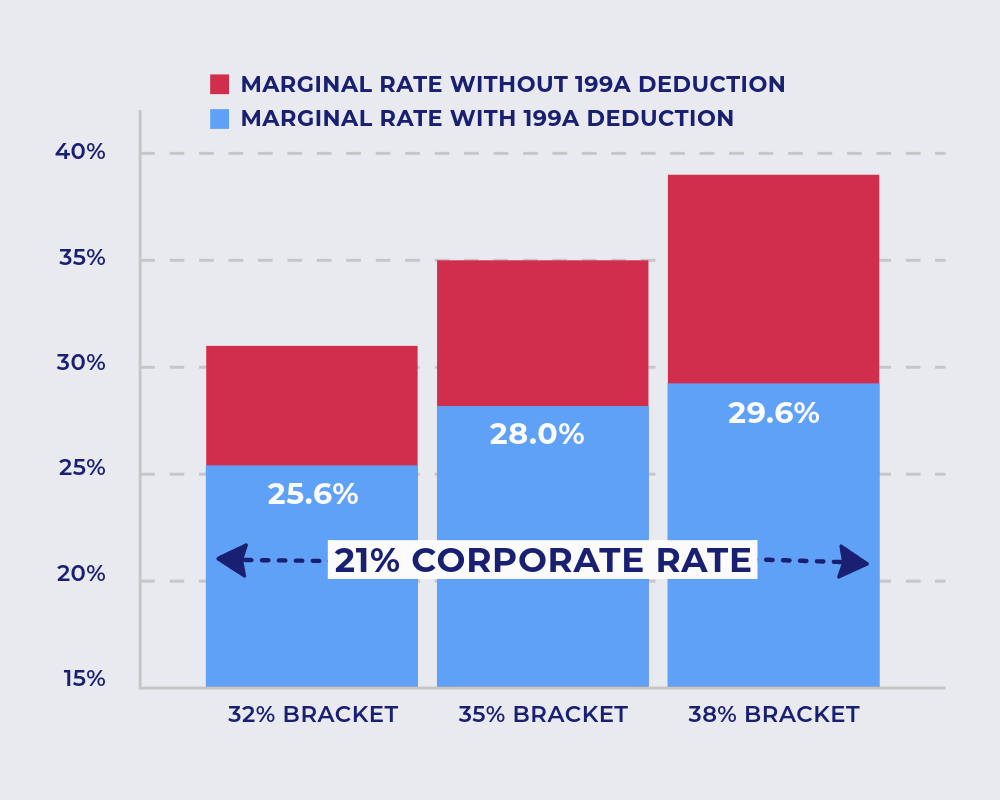

Maintaining Tax Certainty for Main Street

The Issue:

The 2025 tax bill made the 20% 199A deduction permanent, providing much-needed parity and certainty for Main Street businesses.

Why It Matters:

Tax certainty is important to multi-generational, family-owned businesses like beer and beverage distributors, the vast majority of which are organized as S-Corps.

One of the most impactful tax provisions for these local businesses: the 20% pass-through deduction of qualified business income under Section 199A. Maintaining this deduction is essential to:

- Investing in critical new equipment and technology

- Growing employee wages and supporting community initiatives

- Competitiveness, fairness and parity with Wall Street corporations

Congress Should:

- Maintain permanence of the 199A pass-through deduction, which reduces the tax gap between Main Street and Wall Street.

Learn More

Watch a WSJ profile of an NBWA member using the 199A deduction to reinvest in its people, technology and community:

-

Effective Alcohol Regulation

The Issue:

America’s state-based alcohol regulatory system, complemented by federal policy, has produced the world’s safest and most competitive alcohol marketplace. Efforts to undermine this system could erode public safety and consumer choice.

Why It Matters:

Established by the 21st Amendment, America’s successful alcohol regulatory structure carefully balances control and access through a three-tier distribution system of licensed businesses (see above). 135,000 independent beer distribution employees operate within this system, which provides:

Public Safety

- Chain of custody enables product integrity

- Local authority enables communities to decide how alcohol is sold and regulated

Competition

- Suppliers of all sizes — including small, local brewers — have access to the market

- The result: 9,000 breweries and unparalleled consumer choice

Growth

- Efficient collection of more than $65 billion in annual tax revenue

- Over 4.2 million American jobs supported by the beer industry

Legislation to allow the USPS to ship alcohol directly to consumers would undermine this proven system by:

- Bypassing state enforcement and licensing

- Loosening underage drinking protections

- Reducing traceability — critical for recalls

What it won’t do? Resolve USPS funding challenges. In fact, it may even increase costs while adding compliance burdens.

Congress Should:

- Support federal policy that reinforces effective regulation under the 21st Amendment

- Reject the United States Postal Service Shipping Equity Act (H.R.3011)

- House Members should join the 21st Amendment Caucus

-

Federal Hemp Policy

The Issue:

In November 2025, Congress revised the federal definition of hemp that originated in the 2018 farm bill. Absent further action by Congress, the sale of certain intoxicating hemp-derived products is scheduled to be prohibited in November 2026.

NBWA’s Position:

- For more than 90 years, the U.S. alcohol marketplace has been governed by federal and state regulations that effectively protect consumers and oversee industry participants, making America’s alcohol system the safest in the world. Maintaining this effective system remains NBWA’s top priority.

- As some in Congress continue to debate federal policy on intoxicating hemp-derived THC beverages, NBWA remains neutral on current legislative proposals.

Alcohol Policy Provides Guidance for Potential Hemp Regulation

NBWA opposes efforts that would harm the well-established system of federal and state alcohol regulation that has successfully balanced public safety and industry competition for nearly a century.

If federal and state policymakers allow hemp-derived THC beverages to be sold in the marketplace, these beverages should be subject to at least the same or higher standards, safeguards, oversights and regulations that govern the alcohol industry.

Responsible legislation should include, without limitation:

- Defining the product, limiting its concentration, licensing industry members, preventing vertical integration and ensuring the federal government and states have the necessary authority to effectively regulate the product and industry.

- Creating a robust regulatory structure that ensures a responsible marketplace that includes, but is not limited to, comprehensive industry regulations, appropriate product research and meaningful revenue collection in the form of excise taxes.

- This system should also allow a state to appropriately permit, restrict or prohibit how products are manufactured, distributed and sold within its borders.

-

Healthcare Transparency

The Issue:

Lack of transparency in healthcare pricing costs Americans up to $1 trillion annually. It affects:

- Patients using healthcare services

- Employers, such as beer and beverage distributors, that offer healthcare benefits to employees

Why It Matters:

Lack of transparency in healthcare pricing makes it difficult for patients and employers to manage costs. Beer distributors offer competitive healthcare benefits but face dramatic and unpredictable increases in healthcare-related expenses that limit their ability to make additional investments in employees and communities.

The Patients Deserve Price Tags Act (S.2355/H.R.5582) seeks to foster a competitive, consumer-driven healthcare market by:

- Eliminating blind billing

- Ensuring transparent pricing for services

- Giving employers real-time access to their own claims, including fees for intermediaries

Congress Should:

- Cosponsor the Patients Deserve Price Tags Act (S.2355/H.R.5582) , which would require all negotiated rates and cash prices between plans and providers to be publicly accessible.

Learn More

The average employer-sponsored family insurance plan has increased by 50% in the last decade. Learn how this is impacting the beer and beverage distribution industry:

-

Organized Cargo Theft

The Issue:

Organized cargo and retail theft has surged dramatically in recent years, posing safety risks and economic challenges to American communities. It affects:

- Consumers facing higher prices and reduced availability

- Businesses already grappling with a challenging market

- Employees at physical risk

Why It Matters:

Sophisticated criminal enterprises are increasingly targeting cargo and retail, resulting in higher costs for both businesses and consumers, reduced product availability and heightened safety concerns. Beer and beverage distributors are being targeted by criminal groups, harming these local businesses and putting public safety at risk.

The Combating Organized Retail Crime Act (H.R.2853/ S.1404) addresses the evolving and increasingly complex nature of these crimes by:

- Enhancing coordination between federal, state and local law enforcement, including ATF

- Supporting ongoing investigations

- Strengthening penalties for those involved in organized cargo and retail theft

Congress Should:

- Support a floor vote on the Combating Organized Retail Crime Act (H.R.2853/S.1404), which would enhance federal-state coordination and strengthen the legal framework for enforcement.

Learn More

Read about beer and beverage distributors that have been targeted by organized criminal enterprises:

-

Dietary Guidelines Review

The Issue:

The Sober Truth on Preventing Underage Drinking (STOP) Act authorizes the Interagency Coordinating Committee on the Prevention of Underage Drinking (ICCPUD) and federal underage drinking prevention programs through FY 2027. The ICCPUD recently went far beyond its congressional mandate to weigh in on adult alcohol consumption in an effort to influence the 2025-2030 Dietary Guidelines for Americans process.

Why It Matters:

Beer distributors are committed partners in preventing underage drinking and actively support the community coalitions funded under the STOP Act. ICCPUD straying from its statutory mission stretches limited public health resources thinner and weakens congressional oversight.

Congress Should:

- Use authorization and oversight to ensure ICCPUD remains focused on its statutory mission of preventing underage drinking.

-

Tariffs and Trade

The Issue:

The $400 billion American beer industry is directly affected by national trade policy, including new and expanded tariffs on aluminum, steel and imported beverages.

Why It Matters:

America’s 3,000 independent beer distributors carry robust portfolios of both domestic and imported products. The beer industry is also a major user of aluminum and steel, making it sensitive to input costs that can ripple throughout the supply chain and affect both consumers and local businesses.

Congress Should:

- Work with the administration to ensure that tariffs on aluminum, steel and imported beverages do not impose disproportionate costs on independent beer distributors and their customers.

-

TTB Funding

The Issue:

The Alcohol and Tobacco Tax and Trade Bureau (TTB) oversees tax collection, permitting and competition for the entire U.S. beverage alcohol marketplace.

Why It Matters:

An under-resourced TTB creates real operational disruptions for thousands of businesses across the supply chain that depend on it to deliver consistent, effective regulation of the marketplace.

Congress Should:

- Provide adequate funding for TTB in FY 2027 so the agency can effectively administer its alcohol tax and regulatory responsibilities.

-

Revitalizing Local Businesses

The Issue:

Bars, restaurants and entertainment venues impacted by the pandemic continue to face challenges with lower foot traffic and higher operating costs.

Why It Matters:

Energy-efficient draft beer systems provide operational savings while encouraging on-premise spending. Providing tax incentives for draft systems will help bolster the hospitality industry that employs over 16 million Americans.

Congress Should:

- Pass the Creating Hospitality Economic Enhancement for Restaurants and Servers (CHEERS) Act (H.R.3325/S.1732), which provides a tax deduction for bars, restaurants, taprooms and entertainment venues that invest in energy-efficient draft beer systems and related equipment.

-

Multiemployer Pension Plans

The Issue:

The long-term stability of multiemployer-defined benefit pension plans is uncertain. Recent proposals from the Pension Benefit Guaranty Corporation could increase withdrawal liability

Why It Matters:

Beer distributors who participate in these pension plans are committed to meeting their contribution responsibilities. While some of the most troubled plans have been temporarily stabilized after receiving Special Financial Assistance, further action is needed to ensure long-term stability

Congress Should:

- Take action to address withdrawal and partial withdrawal liability in multiemployer pension plans, including PBGC regulatory proposals that could impose disproportionate burdens on small business employers.